With the end of the school and summer holidays behind us, there are increased signs of the UK flex market returning to some degree of normality. Business confidence is returning, but the desire for ongoing flexibility remains high, as reflected in the continued rise in contractual occupancy within flexible office space.

KEY FINDINGS

- Occupancy rates* across the UK are up to 80%, the highest since the pandemic began

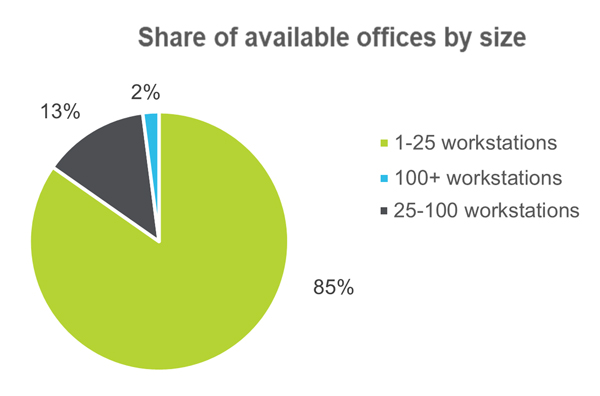

- 85% of available supply caters for small- to mid-sized requirements for clients needing space for between 1 and 25 workstations

- Investment needed in larger flex spaces outside London if it is to become a viable corporate solution

- Flex vacancy rates have declined to pre-pandemic levels based on Instant’s view of the market, whereas according to Savills, traditional office vacancy rates remain high

- Space utilisation within flexible workspaces is currently around 20-40% lower than contractual occupancy

EXECUTIVE SUMMARY

In September, average occupancy rates across the UK rose to 80%, the highest level since the pandemic began. However, although this is a very positive step for the industry, it does mean that the availability of larger spaces is becoming very limited.

The industry appears to be on the road to recovery, but what does this mean for the customer?

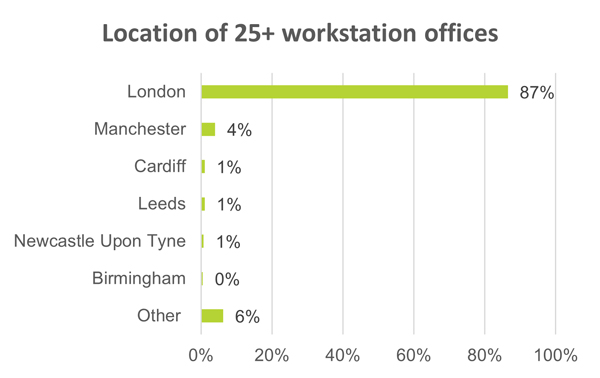

- Larger spaces are in short supply so corporate occupiers need to move quickly, particularly if they are looking outside of London, where just 15% of available offices can accommodate requirements of 25+ people.

- Rising occupancy rates will start to impact pricing in key markets and average rates across London have already seen a 5% incline since Q1 2021. Businesses need to factor this into their planning and decision making before rates start to rise even further.

- High vacancy rates within traditional office buildings present an opportunity for flex operators to expand or enter new markets, resulting in a greater choice of solution for the customer.

- Businesses need a full understanding of when and how each area of the office is being used to ensure it is fit for purpose and delivers value for those who are returning to the office.

A NARROW WINDOW OF OPPORTUNITY

Larger companies are increasingly recognising the benefits of flexible workspace, whether that be for head offices, satellite offices or local drop-in spaces. The ability to adapt at speed is now a key priority for businesses, and this extends to their real estate portfolios. One of the stumbling blocks to companies acquiring large spaces in the flexible market is the lack of availability of larger floor plates.

Despite rising availability during the pandemic, there is still a limited supply of offices with 25-100 workstations, while office space for 100+ workstations is even more scarce, with just 2% of current available stock accommodating this size of requirement.

Operators are starting to respond to the growing demand for larger spaces and some have announced plans to expand their portfolios. However, it will take some time for these new spaces to be available in the market and so it is vital for occupiers of scale to have full market visibility to be able to make informed business decisions. To take larger floor plates and configure these spaces for private offices also represents a risk for many operators.

INVESTMENT FOCUS OUTSIDE THE CAPITAL

In order for flexible workspaces to capitalise on the growing demand for agile space from larger companies, more supply will be needed in order to make it a viable option for them. Moreover, significant investment in flex space outside the capital is needed, as 87% of 25+ workstation offices are currently found within London. This is ideal for larger companies based in the city, but for the growing number of corporate clients wanting to open satellite offices across the UK, the supply is currently not there to service this demand and if these requirements continue to grow, they will soon outpace supply.

For large clients who foresee a requirement for larger flexible workspaces in their future, they need to move quickly to acquire the limited space currently available as it will take time for investment in larger flex spaces to be made outside of London.

FLEX VS TRADITIONAL OFFICES - HOW HAVE THEY WEATHERED THE STORM?

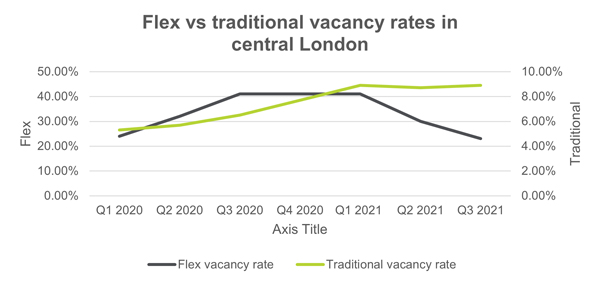

Despite many believing that London offices would stand empty for some time, vacancy rates for flexible office space in central London have already dropped back to pre-pandemic levels. Traditional offices, on the other hand, are still a way off from a full recovery and due to their longer lease terms, some companies may not have yet had the chance to exit their contracts. The future is therefore still uncertain for the traditional office market, and we may see vacancy rates drop further, whereas flexible workspaces appear to be on a steady road to recovery.

High vacancy rates within traditional office buildings do present an exciting opportunity for existing flexible workspace operators and landlords to expand or new players to enter the market in areas where a lack of space has previously restricted growth. However, landlords do now find themselves with more choice. The empty space could spur them to create their own flexible workspace arm to capitalise on the growing need for agility within real estate, or they may decide to partner with an existing flexible workspace provider. Both are routes we are seeing become increasingly of interest and will result in a wider variety of real estate solutions for clients.

IS CONTRACTUAL OCCUPANCY REPRESENTATIVE OF ACTUAL SPACE UTILISATION?

Although contractual occupancy is on the rise, the number of workers utilising the space still has a way to go to catch up. Conversations with our operators indicate that footfall occupancy, or actual space utilisation, is around 20%-40% lower than contractual occupancy. This does vary depending on several factors, including location, amenities, and cost of space. However, one uniting factor is that space utilisation does vary depending on the day of the week, with Tuesday, Wednesday and Thursday unsurprisingly being the busiest days in the office.

Understanding the varying footfall occupancies of offices will enable heads of business to make more educated decisions about their workspaces which can result in cost savings. By adapting the office environment to best suit the way the space is being utilised, companies will entice more employees back into the office and the gap between actual and contractual occupancy will start to close.

CONCLUSIONS

"The strength of the flexible workspace market is becoming apparent as organisations drive for agility within their real estate portfolios. Providing exceptional workspaces for their employees has become a key focus for heads of business, and flexible workspaces facilitate this without the need for long term commitments, allowing businesses to test and evolve."

Lucinda Pullinger, Managing Director UK, The Instant Group

Occupancy rates are on the rise and this trend is being played out across the country, with the UK’s 4 largest cities all showing an increase in occupancy or remaining stable. This is a positive sign for the future of the flex industry across the UK and is a good indicator that many companies see flexible workspaces as a key part of their return-to-work strategy.

As more corporate companies put value on agility, flexible workspace providers will need to turn their focus to investment in larger spaces due to the current shortage of space available to service larger requirements, particularly outside London. This also opens an opportunity for traditional landlords who are facing continued high vacancy rates in their spaces, but the knowledge needed to create a successful flexible space should not be underestimated.

Our view is that this will ultimately be a time of growth for the flexible workspace sector. Diversification in supply will present occupiers with more choice and more solutions, enabling them to find the right solution for their business.

Note: this data is based on Instant’s view of 287 flexible workspaces across the UK.

*Occupancy rates refer to contractual occupancy, the amount of space in the building which is currently under contract with tenants.

Read next

Our experts can deliver insights or a flexible workspace report tailored to your specifications.