Flexible workspaces have become a powerful component of a company’s real estate portfolio, enabling businesses to make value-driven decisions that align with their core values.

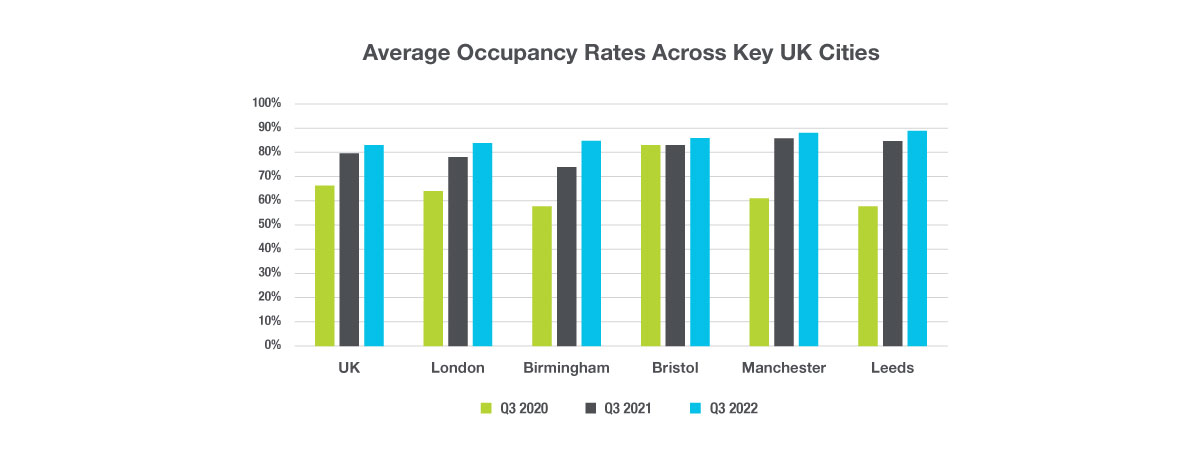

This is resulting in contractual occupancy rates among flexible workspaces in the UK reaching an average of 83% in Q3 this year, the highest level since before the pandemic began. However, this success is not unanimous across the industry, with city centres and high-quality spaces faring better due to shifting occupier priorities. This is opposite to the trend we are seeing within the traditional office sector, where vacancy rates are notably high.

Key insights:

- Occupancy rates in regional cities are above the UK average, with Leeds (89%) and Manchester (88%) seeing the highest rates

- High-quality spaces boast the highest occupancy rates in the UK (88%) as they meet more of the sustainability objectives that clients are demanding

- The move to the suburbs trend that we saw early in the pandemic is now reversing, with occupancy rates in city centres outpacing those in the suburbs as companies place more emphasis on improving the experience of their HQ offices

REGIONAL CITIES TAKE TO THE STAGE

Although occupancy rates within London are on the rise, the highest occupancy rates are currently seen in key regional cities as many companies look to incorporate regional offices into their portfolios. Not only do business hotspots outside the capital provide an opportunity for cost savings, but they also allow companies to tap into new talent pools.

Thanks to its leading universities and diverse population, Manchester is one regional city that’s attracting businesses from across the UK, with traffic to the instantoffices.com’s digital platform indicating that 75% of users looking for flex space within Manchester are based outside the city. This is pushing average occupancy rates up to 88%, one of the highest rates in the country.

The levelling-up agenda

The “levelling-up” agenda that the British government is prioritising also means that economic and political forces are aligning to drive business growth, which is also having a positive impact on occupancy rates within regional cities.

Leeds, for example, has experienced 6% new business growth since before the pandemic, compared to the UK average of 2% over the same period¹. This influx of new businesses makes Leeds a haven for entrepreneurs and start-ups, both of whom drive significant demand for flexible workspaces.

Available space for large occupiers continues to decline

If regional cities want to attract larger occupiers, new investments in spaces that provide large floorplates is needed. Currently, availability of larger spaces of 25+ desks outside London is declining, accounting for just 7% of total available flex supply, down from 11% this time last year. Corporate occupiers who are looking to establish regional business hubs will need to act fast or will otherwise have to wait until new supply enters the market.

OCCUPANCY RATES WITHIN HIGH-QUALITY SPACES ARE HIGHEST IN MARKET

Occupancy rates within high-end spaces are currently the highest in the market, and the gap between quality spaces and cost-effective options is widening. Occupiers are increasingly looking for the very best space available, a key factor in attracting and retaining talent in a world where employees choose to work in places that they think align to their values.

Raising the bar

The desire for high-quality spaces with strong sustainability credentials will ultimately drive supply growth of high-end, premium spaces. This will enable flex supply to meet more of the objectives that clients are demanding, a positive step for ensuring the future strength of the flex industry.

WHAT HAPPENED TO THE HUB-AND-SPOKE MODEL?

At the onset of the pandemic, the hub-and-spoke model was expected to shape the office framework of the future. However, working patterns have evolved differently and the emphasis is now shifting back on the central hub office.

The hub takes on a new role

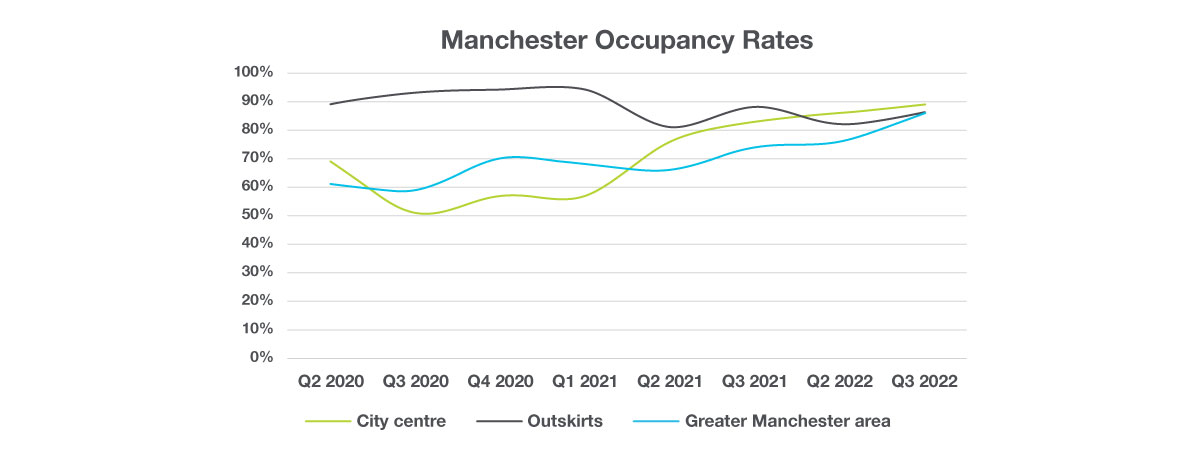

The role of the office is to provide a central location to collaborate and connect with co-workers. As such, companies are continuing to invest heavily in their hub office, creating an experience that workers won’t want to miss. In the UK, occupancy rates in city centres have been outpacing those in suburban areas since early 2022, where most hub or HQ offices are located

No market is showing this trend clearer than Manchester, whose city centre has rebounded extremely strongly in the past 12 months, as shown by the graph above.

This is not to say that suburban offices are becoming redundant; rather,the role and type of use is changing to reflect a more hybrid style of utilisation.

Going forward, a critical element of a successful hub-and-spoke model is that each office delivers the same engaging experience as the central HQ. Instead of competing against each other, every office should be designed to drive the greatest efficiencies and appeal equally to employees.

Suburban expansion is still taking place

Across the UK, operators are continuing to expand their offerings in suburban areas to absorb demand for spoke locations.

For example, IWG recently announced that 90% of new supply will target the suburbs. Other operators are also growing their portfolios in suburban locations largely due to current supply being substandard and in need of investment.

Clockwise, a multi-site flexible workspace provider in the UK, has already expanded their offerings in Manchester and are in the process of doing the same in Leeds. “In today’s world, we see companies are moving to where the talent is, or getting a second, third, site based on their recruitment strategy. Leeds and Manchester are particularly strong, with a highly educated workforce in key growth sectors. With the ‘war for talent’ being so competitive, the working environment has never been more important, with purpose, culture and environment being a key consideration for anyone in the market for a new role. The office proposition is a key piece in getting the right people, and employers are making the investment in higher quality space such as ours,” said Alexandra Livesey, COO, Clockwise.

OCCUPANCY GROWTH WILL ACCELERATE MARKET TRANSFORMATION

While contractual occupancy rates have reached record levels recently and are on an upward trajectory, the average number of staff working from the office reached a national daily average of 31% in October², far below pre-pandemic levels. However, contractual occupancy can be used as a good indicator of shifting occupier trends and should give both occupiers and providers of space confidence about the future.

With occupancy rates within the traditional market currently at 92% and forecast to remain largely stable over the next year³, if flex occupancy rates continue to rise at the current rate, for the first time we will see flex occupancy converge with traditional levels over the next 12-18 months, a sign of the confidence in the flex market.

Methodology

Data within the report is compiled via The Instant Group’s leading flexible workspace data platform Instant Insights. Data is compiled from operators representing over 670 locations across the UK.

Sources

1: UK business counts - ONS October 2022

2: CoStar/Remit Consulting October 2022

3: Cushman & Wakefield United Kingdom Office Marketbeat Q2 2022

Our experts can deliver insights or a flexible workspace report tailored to your specifications.